Capital expenditures and public sector grants

DB Group is one of the largest investors in Germany.

The focus of our capital expenditure activities remains on improving the performance capability, efficiency and quality of our rail infrastructure and expanding our vehicle fleet.

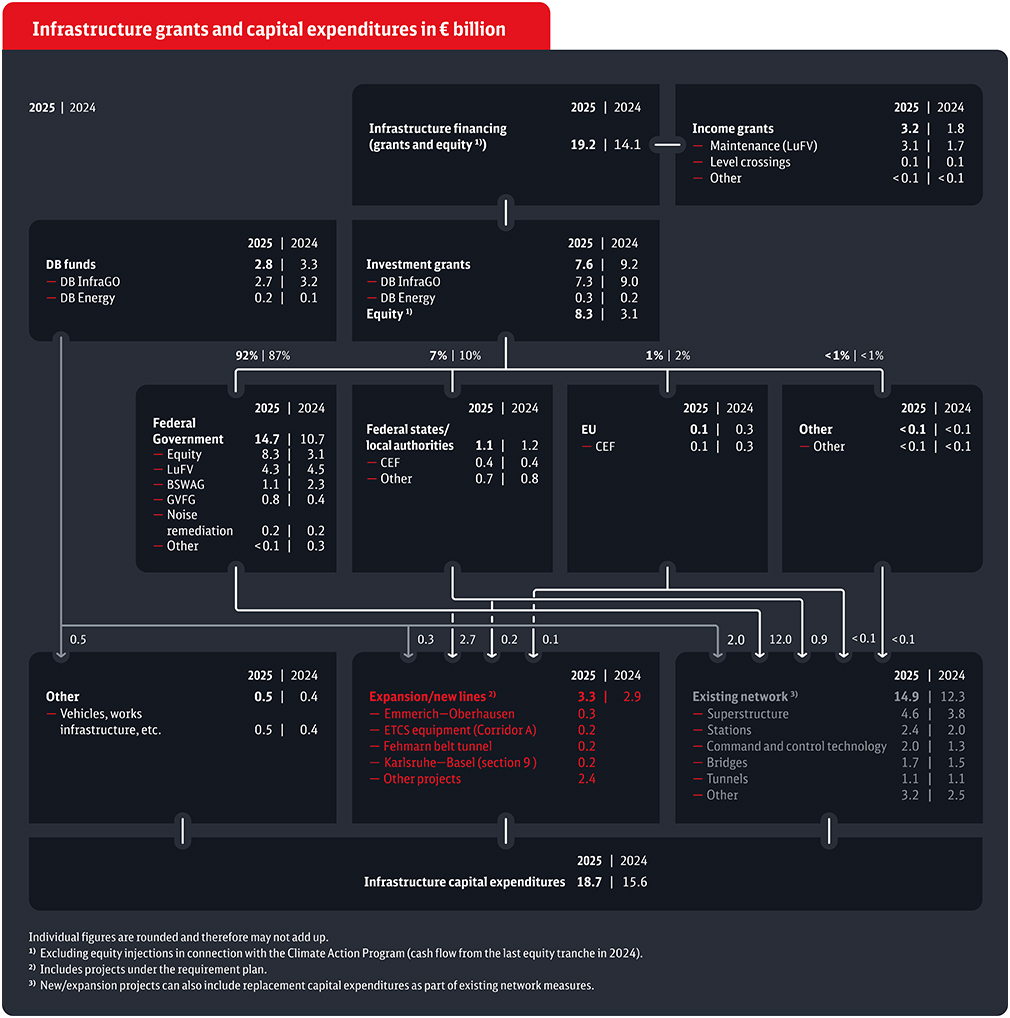

Infrastructure Capital Expenditures

According to Art. 87e (4) of the Basic Law, the Federal Republic of Germany (Federal Government) guarantees that “in the expansion and maintenance of the rail network [...] the common good is to be taken into account.” The Federal Government fulfills this infrastructure mandate by making funds available for capital expenditures. The legal basis is the German Railway Foundation Act and the Federal Rail Infrastructure Expansion Act (BSWAG). The funds are generally granted as non-repayable investment grants for rail infrastructure. We also invest a considerable amount of DB funds. In addition to the investment grants for rail infrastructure, a considerable amount of equity increases in infrastructure have recently been deposited and provided in the Federal budget. In 2024, this amounted to € 5.5 billion. Of this, € 1.125 billion will be used for measures under the Climate Protection Program 2030 and € 4.375 billion for replacement capital expenditures under the Performance and Financing Agreement III (LuFV III). This was contractually agreed between the Federal Government and DB Group in a supplement to LuFV III. The additional equity funds of € 4.375 billion include the redemption of measures pre-financed by DB Group from 2023. The Federal budget for 2025 endowed for equity increases of € 8.314 billion, as well as a loan of € 3 billion for investments in the Federal railway network. Since the amendment of the BSWAG, the Federal Government can also support expenses under certain conditions, in particular for the maintenance and repair of infrastructure.

Investment grants are provided for the acquisition or manufacture of property, plant and equipment.

Below you will find essential information on the various forms of funding and on measures to ensure that these public sector funds are used in accordance with the law.

Investment Grants

Recognition of investment grants in the consolidated financial statements

Investment grants account for by far the largest share of public funds received by DB Group’s infrastructure division. In the 2024 reporting year, the largest share of this was attributable to the DB InfraGO business unit (€ 15.6 billion) and DB Energy (€ 0.3 billion). In DB Group’s accounting system, investment grants are generally deducted from acquisition or manufacturing costs (AMC) on the assets side after completion of the relevant investment. As a result, the investment is recognized at a reduced carrying amount and depreciation is reduced accordingly. The grant thus reduces the operating result over the entire useful life of the investment and is therefore also referred to as a grant with no impact on profit and loss.

In the consolidated financial statements, all capital expenditurs made in a financial year are shown both at their gross value, this means before grants are deducted from assets, and at their net value. In addition, the statement of cash flows shows the receipts of payment from grants received. This also applies to repayments if the funds or the capital expenditures supported by them have not been used in full for the intended purpose. On the one hand, this makes it completely transparent which public sector funds have been collected. On the other hand, the net accounting of investment grants automatically excludes the possibility of an impermissible interest rate request on the publicly financed part of the infrastructure. The capital employed, which forms the basis for calculating the target return, only reflects the net capital expenditures financed from DB Group’s own funds.

The Federal Republic of Germany (Federal Government) is by far the most important provider of grants due to its responsibilities under the Basic Law. At € 14.7 billion, about 92 % of all investment grants in the year 2025 were provided by the Federal Government. The remaining funds came from the Federal states and municipalities (€ 1.1 billion, 7 %), the EU (€ 0.1 billion, 1 %) and other grant providers (< € 0.1 billion, <1 %).

In principle, all public authorities impose strict conditions on the provision of investment grants which ensure that the funds are used in full and for their intended purpose and thus exclude any unauthorized misappropriation or transfer to third parties.

Of the investment grants received by the DB Group in the reporting year (€ 7.5 million), the majority were for infrastructure. The most important sources of funding for investments in infrastructure are grants from the Federal Government, followed by Federal state and municipalities.

The main basis for this was the Federal Railways Expansion Act (BSWAG) and - as a special instrument below the BSWAG - the LuFV. Further investment subsidies were granted under the Municipal Transport Financing Act (GVFG), the Federal Noise Abatement Program and the Railway Crossing Act (EKrG). The European Union grants subsidies for infrastructure investments in the trans-European networks (TEN) (TEN and Connecting Europe Facility [CEF]).

On the balance sheet, investment grants are directly deducted from the purchase and manufacturing costs of the assets to which they relate. The reporting of all grants is such that the competent Federal agencies can conduct comprehensive checks to ensure that they are spent in accordance with their purpose and the law.

In addition to the investment grants, DB Group also received a smaller amount of income grants, which are also mainly attributable to infrastructure. With the amendment to the BSWAG, which came into force on July 9, 2024, the legislature has significantly expanded the possibility for the Federal Government to support expenses in addition to capital expenditures. Agreements must be concluded between the Federal Government and DB Group in order to use the funding options. This took place as part of a supplement to the existing Performance and Financing Agreement (LuFV III) at the end of 2024. The supplement regulates the financing in 2024 and the compensation of pre-financing from 2023.

The extended financing options are listed in Section 11a and include, among other things, the costs of maintenance and repair, costs for IT services in the context of digitization or the equipping of existing vehicles with digital on-board units. Section 11b specifies conditions for the use of funding options in accordance with Section 11a, including the requirement for special justification and the priority use of other funding options outside the BSWAG.

As a special case of modernization or maintenance of the existing network, the new Section 11c BSWAG is dedicated to the concept of general modernization of the high-performance network and lists the 41 corridors individually that will be refurbished in the coming years. It also regulates the financing of rail replacement services that will be required in the course of the general modernization. These will be borne proportionately by the Federal Government (40%), the Federal states (50%) and DB InfraGO (10%).

The European and national requirements of the railway regulation comprise further regulations which also include the monitoring of the use of public funds. In Germany, these are above all the unbundling requirements laid down in the Railway Regulation Act (Eisenbahn-Regulierungsgesetz; ERegG) (Article 7 ff. ERegG), but indirectly also the requirements for fee regulation (§§ 23 ff. ERegG), the monitoring of which is the responsibility of the Federal Network Agency (Bundesnetzagentur; BNetzA).

Of particular relevance here is Article 7 ERegG on separate accounting and the ban on reconciliation of public funds laid down in paragraphs 3 to 5. These clarify that the general obligation to keep separate accounts for railway infrastructure, rail transport and other areas within DB Group also includes the recording of public sector grants. The corresponding separation of accounts and the preparation of annual financial statements (at least balance sheet and statement of income) must also make it clear that public funds received by one of these activities are not transferred to the others.

In monitoring these rules, the BNetzA ensures, among other things, that investment grants are deducted from assets in accordance with these unbundling rules and that all grants received are allocated to the correct areas of activity. The monitoring of the ban on reconciliation also includes checking the appropriateness of internal cost allocation and the regulations on profit and loss transfers.

As part of the regulation of access charges (prices for the use of train-paths, stations, the traction current grid and other service facilities), the BNetzA checks whether subsidies granted to promote one of these areas are actually posted there and deducted from the regulated cost basis in such a way that they benefit infrastructure users.

The latter is automatically guaranteed in the case of on-balance sheet investment grants due to the net accounting described above. In addition, the infrastructure units also receive income grants that are not eligible for capitalization. Such grants are recognized as other revenue and disclosed separately in the annual reports. The BNetzA ensures that these revenues, together with the associated costs, are always allocated and netted appropriately and uniformly in the same division and are thus taken into account in the cost basis for the charges to reduce costs.

As part of the approval of the new grants introduced with Section 11a BSWAG to support maintenance expenses, the EBA must ensure that these are not simultaneously part of the cost base for the access charges approved by the BNetzA in order to rule out double financing.

Federal Government

(1) Federal Rail Infrastructure Extension Act (Bundesschienenwegeausbaugesetz; BSWAG)

The BSWAG is the legal basis for financing federal railway infrastructure. The focus here is on Section 8 of the BSWAG, which regulates the traditional federal subsidies for investments in building new lines or extending existing ones and for replacement investments in existing federal railways. The annex to Section 1 of the BSWAG lists the individual projects to be implemented as part of the "Federal Rail Requirements Plan."

Further details as well as other optional eligibility criteria are regulated in §11 BSWAG.

The Federal Government and DB AG have concluded various multi-year financing agreements to specify the federal funding guaranteed under the provisions of the BSWAG.

(2) LuFV

The Performance and Financing Agreement (Leistungs- und Finanzierungsvereinbarung; LuFV) between the Federal Government and railway infrastructure companies concerns the maintenance of rail lines and financing therefor. To this end, and on the basis of this agreement, the Federal Government makes payments that are exclusively earmarked for the implementation of replacement investments in railway lines (Section 11, paragraph 1 and Section 8, paragraph 1 of the BSWAG), which are known as infrastructure contributions. The first agreement, known as the LuFV I, was valid for the period 2009 to 2014, and was replaced by the LuFV II on 1 January 2015. This was followed on 1 January 2020 by the LuFV III, which was renegotiated with the Federal Government and has a term double that of the LuFV II (ten years, running from 2020 to 2029). The LuFV is based on comprehensive transparency and governance. The Federal Railway Authority (Eisenbahn-Bundesamt; EBA) monitors how the agreement is implemented. There were 17 criteria set out in the LuFV III to measure the success of the agreement. If DB fails to meet its contractual requirements, this is punishable with a fine.

The financing architecture is also to be further developed in connection with the establishment of the common good-oriented infrastructure. In particular, this includes consolidating the existing financing agreements in the existing network (especially the LuFV) into a Performance Agreement (LV) InfraGO.

Until then, the new funding opportunities resulting from the amendment of the Federal Rail Infrastructure Expansion Act (BSWAG) will be implemented through supplementary agreements to the LuFV III. These agreements are intended in particular to finance unforeseen cost increases from previous years, the implementation of corridor refurbishments, the funding of maintenance measures and improvements to station infrastructure, as well as the targeted strengthening of federal oversight. In particular, the third supplementary agreement to LuFV III secured the financing of the railway infrastructure companies’ existing network during the transition period between LuFV III and a new successor agreement (LV InfraGO), planned to take effect from January 1, 2027, for the years 2025 and 2026.

BUV

In order to speed up implementation of the projects in the Requirements Plan, the Plan Implementation Agreement (Bedarfsplanumsetzungsvereinbarung; BUV) concluded between DB and the then Federal Ministry of Transport and Digital Infrastructure (Bundesministerium für Verkehr und digitale Infrastruktur; BMVI) came into force on 1 January 2018. In place of the previous flat-rate planning costs, the Federal Government now funds the total project costs, with the DB Group contributing an amount equal to the economic viability of the project portfolio. The Federal Railway Authority (EBA) has boosted planning support and has made non-compliance with commissioning deadlines subject to penalties.

(3) RV 2020

Where the financing and implementation of investment projects of the Federal Government for infrastructure expansion do not fall within the scope of the LuFV or BUV, a framework financing agreement then applies. A new agreement was concluded between the Federal Government and DB in 2020, which replaces the previous agreement (1999 Framework Agreement). It also regulates the co-financing of eligible costs by the railway infrastructure company, depending on how economically viable the measure is.

(4) Noise remediation

The Federal Government has grants for "noise reduction measures for existing tracks of the federal railways." Subsidies are granted for active noise protection (investments = noise barriers) if the noise level exceeds certain immission values.

(5) Municipal Transport Financing Act (Gemeindeverkehrsfinanzierungsgesetz; GVFG)

These federal subsidies relate to grants from the Federal Government for investments in expansion and new construction projects by DB designed to improve the traffic conditions in municipalities, in the amount of 60 to 90% of the eligible costs. This will support the expansion of existing rail infrastructure and the construction of new rail infrastructure for regional rail passenger transport (Schienenpersonennahverkehr; SPNV). The projects eligible for funding include investments in railway lines to increase capacity and to reactivate or electrify railway lines, as well as investments in refuelling and charging infrastructure for alternative drives. Projects for building and expanding railway stations are also eligible for funding for a limited period until 2030.

(6) European Deployment Plan (EDP)

The EU Member States have committed themselves to gradually equipping trans-European corridors (TEN corridors) with the European Train Control System (ETCS). In order to meet the European equipment obligation, the Federal Government provides federal subsidies through what are known as adjustment agreements (Anpassungsvereinbarungen; APV). Alongside federal funding, the adjustment agreements include additional EU funding.

Federal States/Municipalities

(1) Municipal Transport Financing Act (GVFG)

The state authorities grant subsidies under the Municipal Transport Financing Act (GVFG) to complement the federal funding granted under the GVFG.

(2) Other

Other subsidies from the states/municipalities come from both regionalisation funds and general budgets or are based on the states' and municipalities' own support programmes.

EU

CEF

The EU's most important support scheme for infrastructure funding is the Connecting Europe Facility (CEF). It has been in place since 2014 and will continue in the next multi-annual financial framework from 2021 to 2027. Within the framework of grant funding using CEF funds, the advance and interim payments will be made in the form of reports or applications to CINEA (the European Climate, Infrastructure and Environment Executive Agency) to be submitted by the beneficiaries – in this case the BMDV. The application must confirm that the claimed costs have actually been incurred and that they relate to the benefits attributable to eligible events as defined by the CEF Grant Agreement. This must be verified by the EBA, acting as an independent audit body. CEF not only supports the expansion of infrastructure, including dual-use infrastructure for military mobility, but also, for example, the equipping of vehicles with noise-reduced brakes or ERTMS onboard units.

Other

Grants from other third parties concern investments made by non-public entities, for example private individuals or companies (partnerships or corporations) for investment measures in property, plant and equipment.